If you are involved in setting up financial reports you might face the requirement that one single account needs – depending on its balance – either be included on the asset or liability side of a company’s balance sheet. How this can be realized in Management Reporter is illustrated in the following.

Initial Situation

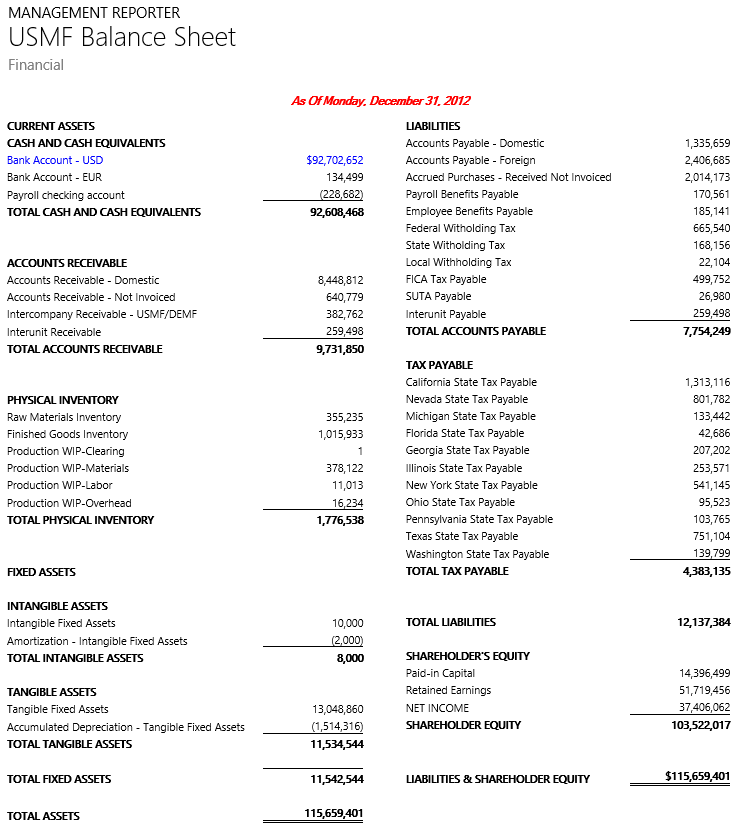

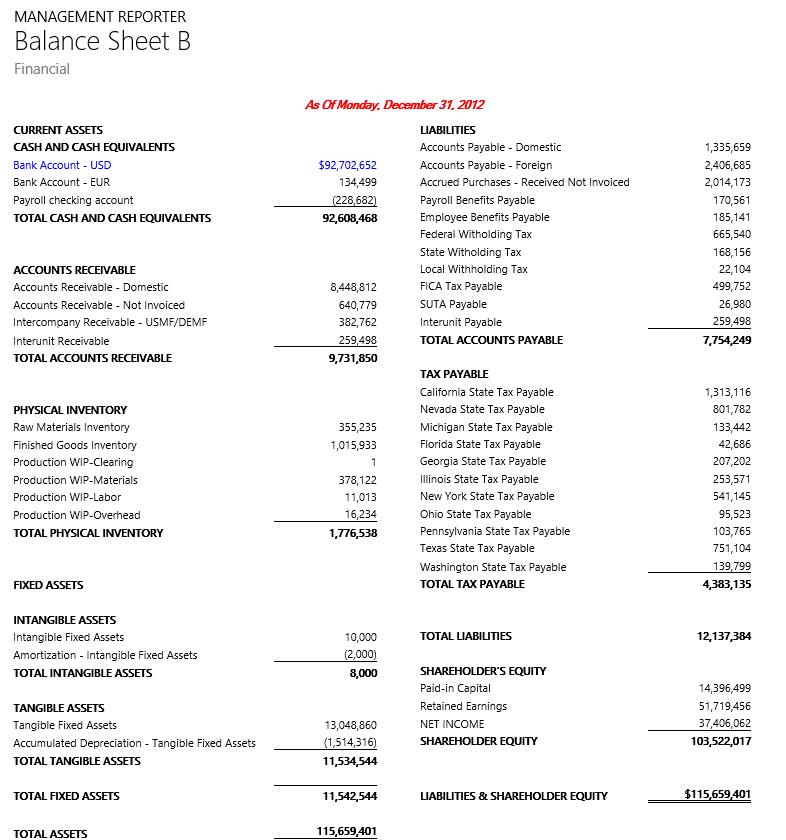

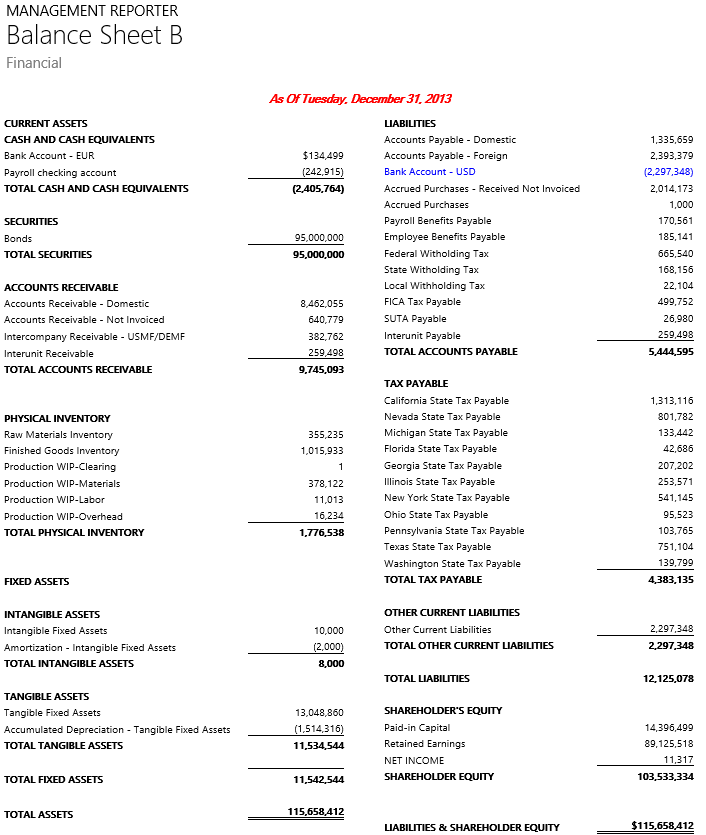

In 2012 the “Bank Account – USD” shows a positive balance of approximately

+93 mio. USD and in 2013 the same account has a negative balance of approximately -2 mio. USD. Using the default balance sheet report that is shipped with Management Reporter results in the following balance sheet reports:

As you can identify from the screenshots above, the bank account is included on the asset side of the balance sheet irrespective of ist balance. To change this illustration, follow these steps:

As you can identify from the screenshots above, the bank account is included on the asset side of the balance sheet irrespective of ist balance. To change this illustration, follow these steps:

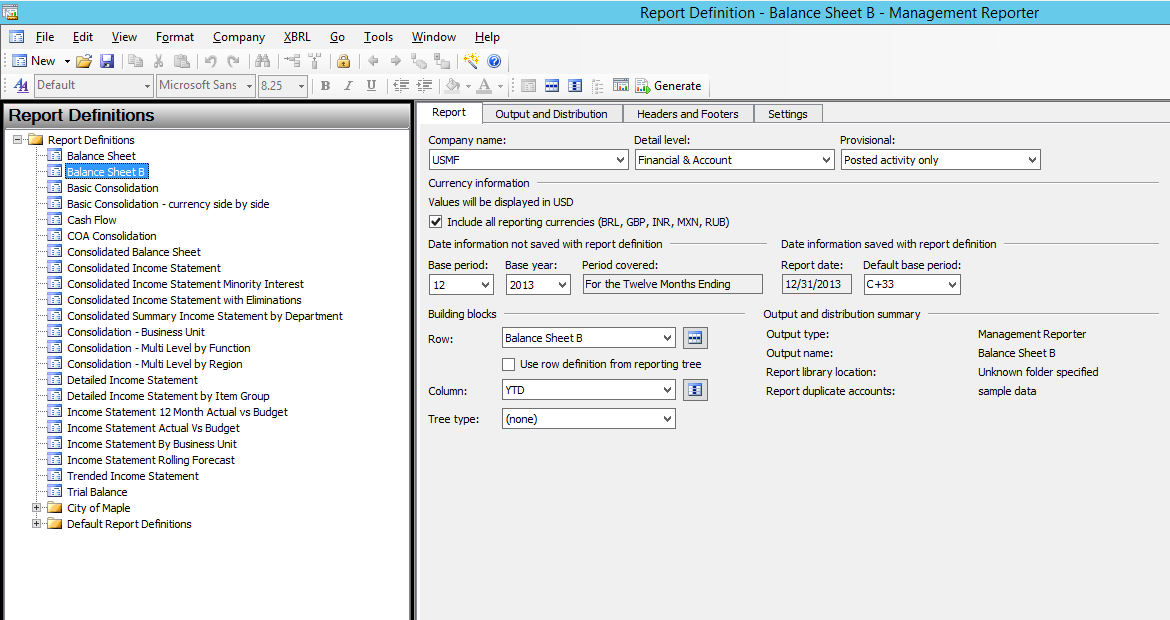

Step 1: Copy the original report

I copy the original report and save it under a different name (Balance Sheet B) to make sure that the original report does not get destroyed by the following changes.

Step 2: Copy the original line structure

I also create a copy of the original line structure and save it under a different name (Balance Sheet B) to make sure that I can always go back to the original line structure in case that something goes wrong.

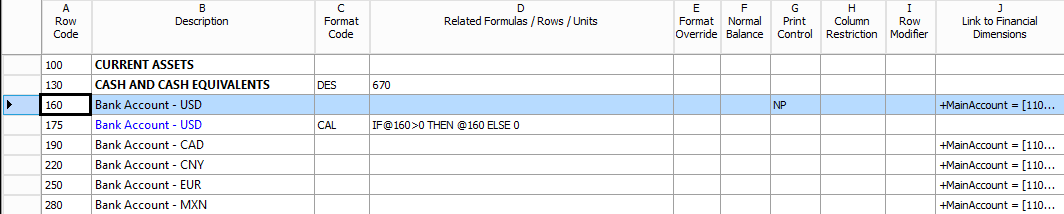

Step 3: Define non-printing line in the newly created line structure

After copying the report and the line structure, I define the original reporting line for my bank account as a non-printing line. This can be identified by the NP code in the print control column. See the following screenshot.

(Hint: double check your total and calculation lines that include the line you defined as non-printing and adjust them as required)

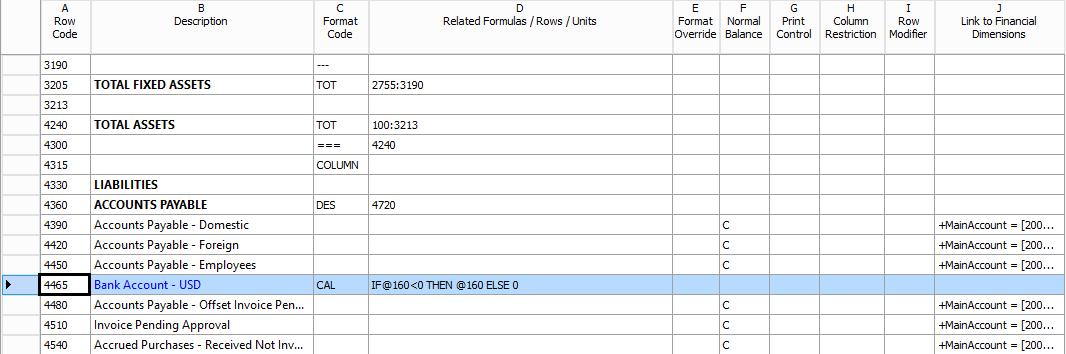

Step 4: Include calculation lines in the newly created line structure

After the original reporting line has been hidden through its definition as a non-printing line, two calculation (CAL) lines are included in the new line structure – one on the asset side of the balance sheet and one on the liability side of the balance sheet. For those calculation lines I use the following IF-THEN-ELSE formulas:

Asset side: IF @160>0 THEN @160 ELSE 0

Liability side: IF @160<0 THEN @160 ELSE 0

Those formulas check whether the balance of the account included in line 160 is positive or negative and depending on the outcome the account is either illustrated on the asset or liability side of my balance sheet.

Outcome

The following two screenshots illustrate the balance sheets in 2012 and 2013.

As one might expect, in 2013 the bank account is included on the liability side of my balance sheet.